, Canada |

3312 |

Not Applicable | ||

(Province or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered | ||

one Common Share at an exercise price of US$11.50 per share |

• |

future financial performance; |

• |

future cash flow and liquidity; |

• |

future capital investment; |

• |

low-priced steel imports, decreased trade regulation, and other trade barriers including tariffs and/or trade wars; |

• |

the Company’s ability to operate the business, remain in compliance with debt covenants and make payments on the Company’s indebtedness, with a substantial amount of indebtedness; |

• |

restrictive covenants in debt agreements limit the Company’s discretion to operate the business; |

• |

significant domestic and international competition; |

• |

macroeconomic pressures such as inflation and interest in the markets in which the Company operates; |

• |

increased use of competitive products; |

• |

a protracted fall in steel prices resulting in reduced revenue and/or further impairment of assets; |

• |

excess capacity, resulting in part from expanded production in China and other developing economies; |

• |

protracted declines in steel consumption caused by poor economic conditions in North America or by the deterioration of the financial position of the Company’s key customers; |

• |

increases in annual funding obligations resulting from the Company’s under-funded Pension Plans and Wrap Plan (each as defined in the AIF); |

• |

supply and cost of raw materials and energy; |

• |

impact of a downgrade in credit rating, including our access to sources of liquidity; |

• |

currency fluctuations, including an increase in the value of the Canadian dollar against the U.S. dollar; |

• |

environmental compliance and remediation; |

• |

unexpected equipment failures and other business interruptions; |

• |

a protracted global recession or depression; |

• |

changes in or interpretation of royalty, tax, environmental, greenhouse gas (“GHG”), carbon, accounting and other laws or regulations, including potential environmental liabilities that are not covered by an effective indemnity or insurance; |

• |

risks associated with existing and potential lawsuits and regulatory actions against the Company; |

• |

impact of disputes arising with our partners; |

• |

the Company’s ability to implement and realize its business plans, including its ability to fully implement, stabilize and optimize electric arc furnace (“EAF”) steelmaking operations and realize the anticipated operational, financial and strategic benefits of the transformation; |

• |

the Company’s ability to operate the EAF and related melt shop and downstream equipment at sustainable production rates consistent with planned capacity, quality specifications and cost performance; |

• |

expected increases in liquid steel capacity and productivity as a result of the transformation to EAF steelmaking; |

• |

expected cost savings associated with the transformation to EAF steelmaking; |

• |

reliance on a single primary steelmaking route following the cessation of blast furnace operations |

• |

the realization, measurement and regulatory recognition of expected reductions in carbon dioxide (“CO₂”) emissions associated with the transition to EAF steelmaking, including impacts on carbon compliance obligations, carbon pricing regimes and government support arrangements such as the Federal SIF EAF Loan (as defined in the AIF); |

• |

the availability, reliability and cost of electrical power required for EAF operations, including the risks that higher cost of internally generated power and market pricing for electricity sourced from our current grid in Northern Ontario could have an adverse impact on our production and financial performance; |

• |

the timing and completion of planned local and regional electricity transmission and distribution infrastructure upgrades necessary to support the Company’s long-term power requirements, including the risk of delays, capacity constraints or changes in project scope; |

• |

the potential for Indigenous rights, claims, consultation requirements or related matters to affect ongoing operations, infrastructure, energy supply arrangements or future development initiatives; |

• |

risks relating to scrap pricing, metallics supply, consumable usage and overall conversion costs; |

• |

access to an adequate supply of the various grades of steel scrap; |

• |

the risks associated with the steel industry generally; |

• |

economic, social and political conditions in North America and certain international markets; |

• |

changes in general economic conditions, including ongoing market uncertainty and global geopolitical instability; |

• |

risks associated with inflation rates; |

• |

risks inherent in the Company’s corporate guidance; |

• |

failure to achieve cost and efficiency initiatives; |

• |

risks inherent in marketing operations; |

• |

risks associated with technology, including electronic, cyber and physical security breaches; |

• |

construction risks, including delays and cost overruns; |

• |

the availability of alternative metallic supply; |

• |

decommissioning and environmental risks associated with closed blast furnace and coke oven facilities |

• |

business interruption or unexpected technical difficulties, including impact of weather; |

• |

counterparty and credit risk; |

• |

labor interruptions and difficulties; and |

• |

changes in capital markets. |

A. |

Undertaking |

B. |

Consent to Service of Process |

EXHIBIT INDEX

SIGNATURE

Pursuant to the requirements of the Exchange Act, Algoma Steel Group Inc. certifies that it meets all of the requirements for filing on Form 40-F and has duly caused this annual report to be signed on its behalf by the undersigned, thereto duly authorized.

Dated: March 11, 2026

| ALGOMA STEEL GROUP INC. | ||

| By: | /s/ Rajat Marwah | |

| Name: Rajat Marwah | ||

| Title: Chief Executive Officer | ||

Exhibit 99.1

ANNUAL INFORMATION FORM

for the twelve month period ended December 31, 2025

Dated: March 11, 2026

TABLE OF CONTENTS

| INTRODUCTION |

1 | |||

| CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION |

1 | |||

| MARKET AND INDUSTRY DATA |

3 | |||

| CORPORATE STRUCTURE |

3 | |||

| DESCRIPTION OF THE BUSINESS |

5 | |||

| RISK FACTORS |

22 | |||

| DIVIDENDS |

51 | |||

| DESCRIPTION OF CAPITAL STRUCTURE |

51 | |||

| MARKET FOR SECURITIES |

58 | |||

| AGREEMENTS WITH SHAREHOLDERS |

60 | |||

| ESCROWED SECURITIES AND SECURITIES SUBJECT TO CONTRACTUAL RESTRICTIONS ON TRANSFER |

61 | |||

| DIRECTORS AND EXECUTIVE OFFICERS |

61 | |||

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS |

69 | |||

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS |

69 | |||

| TRANSFER AGENT, REGISTRAR AND WARRANT AGENT |

69 | |||

| MATERIAL CONTRACTS |

69 | |||

| INTEREST OF EXPERTS |

73 | |||

| ADDITIONAL INFORMATION |

73 | |||

| APPENDIX A CHARTER OF THE AUDIT COMMITTEE |

74 | |||

(i)

ANNUAL INFORMATION FORM

INTRODUCTION

Unless otherwise indicated, all references in this annual information form (the “Annual Information Form”) to “Algoma,” “we,” “our,” “us,” “the Company” or similar terms refer to Algoma Steel Group Inc. and its consolidated subsidiaries.

We publish our consolidated financial statements in Canadian dollars. In this Annual Information Form, unless otherwise specified, all monetary amounts are in Canadian dollars, all references to “C$” mean Canadian dollars and all references to “$” or “US$” mean U.S. dollars. Unless otherwise indicated, the information contained herein is given as at December 31, 2025.

Effective November 5, 2024, the Company’s board of directors approved a change in the Company’s fiscal year-end from March 31 to December 31, effective as of December 31, 2024. Unless otherwise indicated in this Annual Information Form, all references to: “fiscal 2025” are to the twelve month period ended December 31, 2025, the fiscal year ended December 31, 2024 is referred to as the “nine month period ended December 31, 2024”, and “fiscal 2024” are to the twelve month period ended March 31, 2024.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION

This Annual Information Form contains “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 and “forward-looking information” under applicable Canadian securities legislation (collectively, “forward-looking statements”), that are subject to risks and uncertainties. These forward-looking statements include information about imposed and threatened tariffs, including the impact, timing and resolution thereof, possible or assumed future results of our business, financial condition, results of operations, liquidity, plans and strategic objectives, Algoma’s expectation to pay a quarterly dividend, the expected timing of the EAF (as defined below) transformation and the resulting increase in raw steel production capacity and reduction in carbon emissions. In some cases, you can identify forward-looking statements by the words “believe,” “project,” “expect,” “anticipate,” “estimate,” “intend,” “strategy,” “future,” “opportunity,” “plan,” “pipeline,” “may,” “should,” “will,” “would,” “will be,” “will continue,” “will likely result” or the negative of these terms or other similar expressions. In addition, any statements that refer to expectations, intentions, projections or other characterizations of future events or circumstances contain forward-looking information. Statements containing forward-looking information are not historical facts but instead represent management’s expectations, estimates and projections regarding future events or circumstances. In addition, our business and operations involve numerous risks and uncertainties, many of which are beyond our control, which could result in our expectations not being realized or otherwise materially affect our financial position, financial performance and cash flows. Although management believes that expectations reflected in forward-looking statements are reasonable, such statements involve risks and uncertainties and should not be regarded as a representation by the Company or any other person that the anticipated results will be achieved. The Company cautions you not to place undue reliance upon any such forward-looking statements, which speak only as of the date they are made. Our forward-looking statements are not guarantees of future performance, and actual events, results and outcomes may differ materially from our expectations suggested in any forward-looking statements due to a variety of factors, including, among others, those set forth in the section entitled “Risk factors.” Although it is not possible to identify all of these factors, they include, among others, the following:

| • | future financial performance; |

| • | future cash flow and liquidity; |

| • | future capital investment; |

- 2 -

| • | low-priced steel imports, decreased trade regulation, and other trade barriers including tariffs and/or trade wars; |

| • | our ability to operate our business, remain in compliance with debt covenants and make payments on our indebtedness, with a substantial amount of indebtedness; |

| • | restrictive covenants in debt agreements limit our discretion to operate our business; |

| • | significant domestic and international competition; |

| • | macroeconomic pressures such as inflation and interest rates in the markets in which we operate; |

| • | increased use of competitive products; |

| • | a protracted fall in steel prices resulting in reduced revenue and/or impairment of assets; |

| • | excess capacity, resulting in part from expanded production in China and other developing economies; |

| • | protracted declines in steel consumption caused by poor economic conditions in North America or by the deterioration of the financial position of our key customers; |

| • | increases in annual funding obligations resulting from our under-funded Pension Plans and Wrap Plan (each as defined herein); |

| • | supply and cost of raw materials and energy; |

| • | impact of a downgrade in credit rating, including our access to sources of liquidity; |

| • | currency fluctuations, including an increase in the value of the Canadian dollar against the U.S. dollar; |

| • | environmental compliance and remediation; |

| • | unexpected equipment failures and other business interruptions; |

| • | a protracted global recession or depression; |

| • | changes in or interpretation of royalty, tax, environmental, greenhouse gas (“GHG”), carbon, accounting and other laws or regulations, including potential environmental liabilities that are not covered by an effective indemnity or insurance; |

| • | risks associated with existing and potential lawsuits and regulatory actions against the Company; |

| • | impact of disputes arising with our partners; |

| • | our ability to implement and realize our business plans, including our ability to fully implement, stabilize and optimize electric arc furnace (“EAF”) steelmaking operations and realize the anticipated operational, financial and strategic benefits of the transformation; |

| • | our ability to operate the EAF and related melt shop and downstream equipment at sustainable production rates consistent with planned capacity, quality specifications and cost performance; |

| • | expected increases in liquid steel capacity and productivity as a result of the transformation to EAF steelmaking; |

| • | expected cost savings associated with the transformation to EAF steelmaking; |

| • | reliance on a single primary steelmaking route following the cessation of blast furnace operations; |

| • | the realization, measurement and regulatory recognition of expected reductions in carbon dioxide (“CO₂”) emissions associated with the transition to EAF steelmaking, including impacts on carbon compliance obligations, carbon pricing regimes and government support arrangements such as the Federal SIF EAF Loan (as defined herein) |

| • | the availability, reliability, and cost of electrical power required for EAF operations, including the risks that higher cost of internally generated power and market pricing for electricity sourced from our current grid in Northern Ontario could have an adverse impact on our production and financial performance; |

| • | the timing and completion of planned local and regional electricity transmission and distribution infrastructure upgrades necessary to support the Company’s long-term power requirements, including the risk of delays, capacity constraints or changes in project scope; |

| • | the potential for Indigenous rights, claims, consultation requirements or related matters to affect ongoing operations, infrastructure, energy supply arrangements or future development initiatives; |

| • | risks relating to scrap pricing, metallics supply, consumable usage and overall conversion costs; |

| • | access to an adequate supply of the various grades of steel scrap; |

| • | the risks associated with the steel industry generally; |

| • | economic, social and political conditions in North America and certain international markets; |

| • | changes in general economic conditions, including ongoing market uncertainty and global geopolitical instability; |

| • | risks inherent in the Company’s corporate guidance; |

- 3 -

| • | failure to achieve cost and efficiency initiatives; |

| • | risks inherent in marketing operations; |

| • | risks associated with technology, including electronic, cyber and physical security breaches; |

| • | construction risks, including delays and cost overruns; |

| • | our ability to enter into contracts to source steel scrap and the availability of steel scrap; |

| • | the availability of alternative metallic supply; |

| • | the Company’s expectation to declare and pay a quarterly dividend; |

| • | decommissioning and environmental risks associated with closed blast furnace and coke oven facilities; |

| • | business interruption or unexpected technical difficulties, including impact of weather; |

| • | counterparty and credit risk; |

| • | labour interruptions and difficulties; and |

| • | changes in capital markets. |

The preceding list is not intended to be an exhaustive list of all of our forward-looking statements. The forward-looking statements are based on our beliefs, assumptions and expectations of future performance, taking into account the information currently available to us. These statements are only predictions based upon our current expectations and projections about future events. There are important factors that could cause our actual results, levels of activity, performance or achievements to differ materially from the results, levels of activity, performance or achievements expressed or implied by the forward-looking statements. In particular, you should consider the risks provided under “Risk Factors” in this Annual Information Form.

You should not rely upon forward-looking statements as predictions of future events. Although we believe that the expectations reflected in the forward- looking statements are reasonable, we cannot guarantee that future results, levels of activity, performance and events and circumstances reflected in the forward-looking statements will be achieved or will occur. Despite a careful process to prepare and review the forward-looking information, there can be no assurance that the underlying assumptions will prove to be correct. Except as required by law, we undertake no obligation to update publicly any forward-looking statements for any reason after the date of this Annual Information Form, to conform these statements to actual results or to changes in our expectations.

MARKET AND INDUSTRY DATA

Market and industry data presented in this Annual Information Form was obtained from third-party sources and industry reports and publications, websites and other publicly available information, including Statistics Canada, as well as industry and other data prepared by us or on our behalf on the basis of our knowledge of the markets in which we operate, including information provided by suppliers, partners, clients and other industry participants. We believe that the market and economic data presented in this Annual Information Form is accurate and, with respect to data prepared by us or on our behalf that our estimates and assumptions are currently appropriate and reasonable, but there can be no assurance as to the accuracy or completeness thereof. The accuracy and completeness of the market and economic data presented in this Annual Information Form are not guaranteed and we do not make any representation as to the accuracy of such data. Actual outcomes may vary materially from those forecasts in such reports or publications, and the prospect for material variation can be expected to increase as the length of the forecast period increases. Although we believe it to be reliable, we have not independently verified any of the data from third-party sources referred to in this Annual Information Form, analyzed or verified the underlying studies or surveys relied upon or referred to by such sources, or ascertained the underlying market, economic and other assumptions relied upon by such sources. Market and economic data is subject to variations and cannot be verified due to limits on the availability and reliability of data inputs, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in any statistical survey.

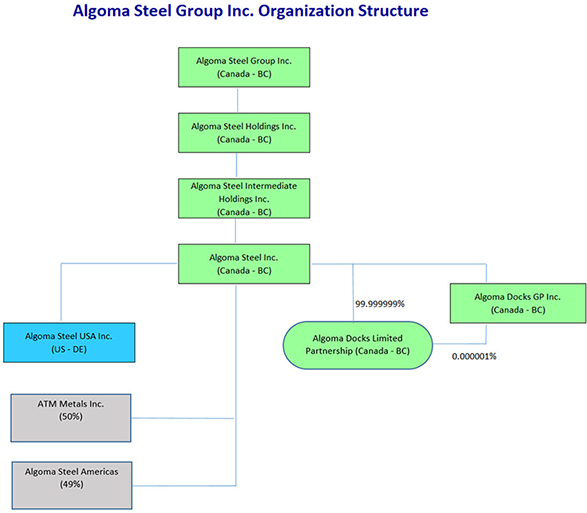

CORPORATE STRUCTURE

Name, Address and Incorporation

Algoma, a corporation organized under the Business Corporations Act (British Columbia) (the “BCA”) in March 2021, is the parent holding company of Algoma Steel Inc., our operating company (“Opco”). Opco was incorporated

- 4 -

in 2016 for the purpose of purchasing substantially all of the operating assets and liabilities of Essar Steel Algoma Inc. (“Old Steelco”) and its subsidiaries in connection with Old Steelco’s restructuring (the “Restructuring Transaction”) under the Canadian Companies’ Creditors Arrangement Act (the “CCAA”). The Restructuring Transaction was completed on November 30, 2018. Prior to November 30, 2018, Opco had no operations, and was capitalized with one common share with a nominal value. On October 19, 2021, Algoma consummated a business combination with Legato, a special purpose acquisition company, and became a publicly traded company with its common shares (the “Common Shares”) and warrants to purchase Common Shares (the “IPO Warrants”) trading on each of the Toronto Stock Exchange (the “TSX”) (under the symbols “ASTL” and “ASTL.WT”, respectively) and The Nasdaq Select Global Market (“Nasdaq”) (under the symbols “ASTL” and “ASTLW”, respectively).

Our principal office is located at 105 West Street, Sault Ste. Marie, Ontario P6A 7B4, Canada and our telephone number is (705) 945-2351. Our website address is www.algoma.com. Information contained on, or accessible through, our website is not a part of this disclosure document and the inclusion of our website address in this document is an inactive textual reference.

Intercorporate Relationships

The following diagram illustrates the inter-corporate relationships between the Company and its material subsidiaries (which are all wholly owned by the Company) as at the date of this Annual Information Form:

- 5 -

Description of the Business

Algoma is a producer of hot and cold rolled steel products, including coiled sheet and plate, located on the Great Lakes in Sault Ste. Marie, Ontario, Canada. The Company is a flat-rolled steel producer in North America and the only producer of discrete plate in Canada, with an estimated annual liquid steel production capacity of approximately 2.8 million tons as of December 31, 2025. Algoma supplies customers primarily in the automotive, construction, energy, defense and manufacturing sectors.

The Company currently operates one EAF. Construction of a second EAF is expected to be completed in the first half of 2026, with commissioning and ramp-up anticipated thereafter. The transition to EAF steelmaking has replaced production from Blast Furnace No. 7, which was decommissioned in January 2026. Blast Furnace No. 6 remains idled.

Algoma’s downstream facilities include its Direct Strip Production Complex (“DSPC”) for production of sheet steel products, constructed in 1995 at an approximate cost of C$450 million, and which integrates continuous casting and hot rolling. We also operate Canada’s only discrete plate rolling mill, which is 166 inches wide, as well as discrete plate heat treating.

The Company’s sheet steel products include a wide variety of widths, gauges and grades, and are available in unprocessed form as hot rolled coil (“HRC”). Primary end users of sheet products include service centers, automotive, manufacturing, construction and tubular industries. Sheet steel products represented approximately 77% of the Company’s total steel shipment volumes for the twelve-month period ended December 31, 2025. As of December 31, 2025, the Company had idled its cold mill facilities, including pickling, hot rolled steel tempering, cold reduction rolling and annealing operations.

Recent modernization of the 166-inch wide plate mill is expected to support annual plate capacity of approximately up to 700,000 tons. In 2024, we completed a modernization of our plate mill, which has allowed us to increase capacity and further improve product quality and capability, which we believe will allow us to optimize margins by the sale of premium quality plate products, and build on our market position as the only domestic discrete plate producer in the Canadian market. Our plate steel products consist of various carbon-manganese, high-strength and low-alloy grades, and are sold in the as-rolled condition as well as subsequent value-added heat-treated conditions. The primary end-user of our plate products is the fabrication industry, which uses our plate products in the manufacture or construction of railcars, buildings, bridges, off-highway equipment, storage tanks, ships, defense and military applications (including armored plate), large diameter pipelines and power generation equipment. Plate steel products have represented approximately 23% of our total steel shipment volumes in the twelve month period ended December 31, 2025.

We sell our finished products to a geographically diverse customer base across North America. For the twelve month period ended December 31, 2025, our shipment volume by product category, geography and end markets were as follows:

|

Twelve month period ending December 31, 2025 Product Shipment Mix |

Twelve month period ending December 31, 2025 Geographic Shipments |

|||||||||||

| Product | Volume | Country | Volume | |||||||||

| Hot Roll | 70% | United States | 51% | |||||||||

| Cold Roll | 7% | Canada | 48% | |||||||||

| Plate | 23% | Mexico | 1% | |||||||||

- 6 -

| End Market Volume | |||||||||||||||

|

Segment |

|

Twelve month period ended Decemeber 31, 2025 |

|

Nine month period ended Decemeber 31, 2024 |

|

Twelve month period ended March 31, 2024 |

|||||||||

|

Transportation1 |

27% | 41% | 43% | ||||||||||||

|

Manufacturing and Construction |

21% | 28% | 30% | ||||||||||||

|

Tubular |

13% | 13% | 10% | ||||||||||||

|

Distribution |

39% | 18% | 17% | ||||||||||||

|

Total |

100% | 100% | 100% | ||||||||||||

1Includes 35-40% automotive

Corporate Strategy and Culture

Our corporate strategy aims to maximize stakeholder value through strategic investments in our business that provide and enhance a sustainable competitive cost position. Key investments include our EAF transformation, the modernization of our plate mill and our completed Ladle Metallurgy Furnace No. 2 (“LMF2”) investment. Through these strategic initiatives, we are seeking to ensure the long-term success and growth of our business. We anticipate that these investments will enhance our leading presence in the Canadian market and allow us to actively contribute to a more sustainable and environmentally responsible steel industry. In addition to the above, we are committed to fostering an entrepreneurial culture within our organization. This culture is rooted in values such as safety, productivity, and a caring attitude, which guide our decisions and interactions. Safety is our top priority, ensuring the well-being of our employees and stakeholders at all times. Productivity is pursued through a culture of continuous improvement, empowering our teams to innovate and optimize processes, resulting in increased efficiency and operational excellence. Lastly, a caring attitude permeates our organization, promoting a supportive and inclusive environment where everyone feels valued and respected. By nurturing this entrepreneurial culture, we aim to foster a strong sense of ownership and accountability among our employees, driving our business towards long-term success while prioritizing the well-being of our people and the communities we serve.

EAF Transformation

On November 10, 2021, our board of directors authorized the Company to construct two state-of-the-art EAFs to replace our existing Blast Furnace No. 7 steelmaking operations (the “EAF Transformation”). The EAF Transformation is expected to reduce our annual carbon emissions by approximately 70%. EAF steelmaking is a method of producing steel by melting scrap metal and other metallic inputs using an electric arc, and is widely used in modern steel production. Our EAF steelmaking facility is being built on vacant land adjacent to our current steelmaking facility to mitigate disruption to current operations, and will be integrated into existing downstream equipment and facilities, thereby reducing capital expenditure requirements.

In early July 2025, the Company achieved its first steel production at Unit One of the EAFs as well as successful electric arc testing and tuning, including individual and tandem tests of all nine Q-One transformer modules. This was a major operational and strategic milestone that marks the start of a new era for Algoma, positioning the Company to produce Volta™, our proprietary green steel brand, at scale. It reflects the successful execution of a key phase in the EAF Transition and demonstrates the performance of the technology platform that underpins our decarbonization strategy. With EAF production now underway, Algoma is advancing toward a more flexible, cost-effective, and environmentally responsible steelmaking model that supports long-term shareholder value.

The Company had planned to continue blast furnace production through 2027 during a staged transition to EAF steelmaking. However, beginning in early 2025 and intensifying in June 2025, unprecedented USA tariff measures and escalating trade tensions with the United States materially and adversely affected the North American steel market. These measures included substantial tariffs on direct steel imports into the United States as well as on certain derivative and downstream steel-containing products.

- 7 -

The scope and magnitude of these trade actions was unprecedented and fundamentally disrupted the Company’s established U.S. sales channels. In addition, tariffs on derivative products reduced demand for Canadian-manufactured finished goods exported into the United States, which in turn materially impacted domestic Canadian steel demand. The combined effect was a material contraction in addressable markets for the Company’s integrated blast furnace production. These external market conditions represented a fundamental change to the commercial assumptions underlying continued operation of the Company’s integrated blast furnace and coke oven facilities. As a result, sustained operation of these facilities became unviable. Accordingly, the Company was required to accelerate the wind-down of blast furnace steelmaking operations and ceased production through this route shortly after December 31, 2025. The Company is now relying on liquid steel production from the EAF.

Ramp-up activities for the EAF Transformation are progressing in line with expectations. The Unit One furnace and associated melt shop assets are performing as designed, with quality metrics achieved across a range of plate and hot-rolled coil product grades. The Q-One power system and other key process components have demonstrated stable and reliable performance, supporting consistent metallurgical quality and process control. Operations are currently running on a full 24-hour-per-day schedule.

The EAF Transformation also includes installation of vacuum tank degassing for steel used in plate products. Vacuum tank degassing offers several significant benefits for steel plate products, including reduced hydrogen content crucial for improving the steel’s resistance to cracking and brittleness, improved cleanliness to reduce impurities and inclusions leading to better surface finish and enhanced mechanical properties, and enhanced homogeneity promoting a more uniform distribution of alloys within the steel to improve consistency and reduce localized variations in properties. Construction is ongoing with the aim of commissioning in mid 2026.

The Company’s Response to Tariffs

The current President of the United States has issued various executive orders imposing tariffs on products imported from Canada. These include tariffs under the International Emergency Economic Powers Act (“IEEPA Tariffs”), applying a 25% duty on most imports from Canada, with a reduced 10% rate on energy products; and tariffs under Section 232 of the Trade Expansion Act of 1962 (“S232 Tariffs”), imposing a 25% ad valorem tariff on all steel and aluminum articles and their derivatives, without exclusions. The tariffs were effective March 4, 2025, paused on March 6, 2025, and then reinstated March 12, 2025. On April 2, 2025, the President announced a minimum 10% tariff (“Reciprocal Tariffs”) on all U.S. imports, effective April 5, 2025 and higher tariffs on imports from 57 countries. Canada was excluded from the application of Reciprocal Tariffs, and the order further clarified that the IEEPA Tariffs and S232 Tariffs would not aggregate on Canadian goods compliant with the United States-Mexico-Canada Agreement (“USMCA”). On June 4, 2025, the tariffs under S232 Tariffs were increased to 50% for all steel and aluminum imports to the United States. At present, the Company is only subject to the S232 Tariffs that imposes a 50% tariff on steel the Company imports into the United States. The ruling by the Supreme Court of the United States on February 20, 2026 regarding the IEEPA Tariffs does not impact the S232 Tariffs.

The ongoing tariffs and trade uncertainty has contributed to volatility in steel demand and pricing in both the U.S. and Canadian markets, with concerns over supply chain disruptions leading to fluctuations in purchasing patterns. Additionally, the uncertainty surrounding trade policies has affected the U.S. dollar exchange rate, which in turn impacts the Company’s sales and cost structure by influencing raw material costs, pricing competitiveness, and cross-border trade dynamics. In most cases, it is not feasible for the Company to pass on the tariff cost to its customers. Unlike the U.S. market which is predominantly contract-based, the Canadian steel market is more focused on spot transactions. As a result, the Company has been experiencing an increasing demand and pricing imbalance between the U.S. and Canadian markets, resulting in Canadian transactional pricing below U.S. pricing, which we expect is due to the increased supply of the Canadian market from domestic producers, the continuance of steel shipped into Canada by U.S. steel manufacturers and increased import offers from other countries priced at less-than-fair-value. During the three month period ended December 31, 2025 the Company’s Average Net Sales Realization (“NSR”), defined as steel revenue less freight revenue per steel tons shipped, for Canadian sales was up to 40% lower than its U.S. results across many product categories. This is a significantly greater discrepancy than historical averages and resulted in approximately C$27.0 million lower revenue on Canadian sales during the three month period ended December 31, 2025. During the three and twelve month periods ended December 31, 2025, the Company incurred tariff costs of C$60.6 million and C$225.0 million, respectively. During the three and twelve month periods ended

- 8 -

December 31, 2025, steel shipments to the United States represented 45% and 51% of total steel shipments, respectively.

The S232 Tariffs in the United States have effectively closed the US market to Canadian steel producers, and resulted in an oversupply of steel coil in Canada, significantly influencing the selling price of domestic steel coil in Canada. The resulting price volatility and trade uncertainty has fundamentally disrupted the business model for Canadian steel production.

On September 28, 2025, in response to sustained market disruption, volatility and uncertainty arising from prolonged and expanded tariff measures, the Company’s board of directors approved a plan to accelerate the wind-down and decommissioning of the Company’s blast furnace and coke oven operations and transition fully to EAF steelmaking. In connection with this plan, on December 1, 2025, the Company issued layoff notices (the “Layoffs”) to 1,005 unionized employees, effective March 23, 2026. The Layoffs resulted in expected severance costs totaling C$45.8 million, which were recognized in the consolidated statements of net loss for the and twelve-month period ended December 31, 2025. To align production with prevailing market conditions, the Company intends to focus on the manufacturing and sale of discrete plate and to scale back coil production, with predominant emphasis on the Canadian market. As EAF production ramps up, the Company expects to align product offerings with domestic demand. As a result of the tariff measures and the resulting market disruption, the Company provided notice to certain primary raw material suppliers and customers asserting that these unforeseen trade measures have fundamentally altered the commercial basis of certain agreements. The Company has initiated, and is responding to, related legal proceedings in connection with certain supply agreements, including proceedings concerning the Company’s position that certain agreements have been frustrated. The Company believes it has valid legal remedies and defenses in these matters and intends to defend its position. Management continues to monitor these proceedings and will recognize provisions where a present obligation exists and a reliable estimate of loss can be made in accordance with applicable accounting standards.

The Company is further exploring liquidity tools and funding programs that could support its current operations and enable strategic diversification of products, including the LETL Facilities, as defined and described further below.

LETL Facilities

On November 14, 2025, the Company entered into agreements with Canada Enterprise Emergency Funding Corporation under the Large Enterprise Tariff Loan program and the Ministry of Northern Economic Development and Growth to secure a C$500 million governmental loan comprised of a C$400 million loan facility from the Government of Canada and a C$100 million loan facility from the Province of Ontario (collectively, the “LETL Facilities”). The LETL Facilities are provided proportionately for which 20% is secured, ranking junior to the Company’s existing first lien Revolving Credit Facility and its 9.125% Senior Secured Lien Notes, with the remaining 80% of the Facilities being unsecured. The LETL Facilities have a seven-year term, with interest at CORRA + 200 bps for the first three years, stepping up by 200 bps each year thereafter, and include customary positive and negative covenants, including a restriction on capital distributions.

In connection with the LETL Facilities, the Company issued 6,768,953 Common Share purchase warrants (the “LETL Warrants”) to Canada Enterprise Emergency Funding Corporation (5,415,162 LETL Warrants) and His Majesty the King in Right of Ontario (1,353,791 LETL Warrants). Each LETL Warrant is exercisable for one Common Share at an exercise price of $11.08, vesting proportionately as unsecured draws are made and subject to customary anti-dilution adjustments in the event of share reorganizations, rights offerings, distributions or certain other corporate transactions. The LETL Warrants have a term expiring at 5:00 p.m. (Toronto time) on November 14, 2035, unless earlier repurchased, exercised or terminated in accordance with their terms. The Company also retains certain rights to repurchase the LETL Warrants following repayment of the LETL Facility.

For further details please refer to “Material Contracts - LETL Facilities”.

- 9 -

IPO Warrants

On October 19, 2021, Algoma consummated a business combination with Legato, a special purpose acquisition company, and its common shares and the IPO Warrants became listed on the TSX and Nasdaq. The IPO Warrants and LETL Warrants are referred to collectively in this Annual Information Form as Warrants (the “Warrants”), unless context otherwise requires or as specifically states.

DSPC Production Process

Our DSPC hot mill provides a cost advantage over the traditional integrated hot rolling manufacturing process. Current annualized production capacity of the DSPC complex is 2.3 million tons.

A hot strip mill coupled to direct casting can provide a significant competitive advantage in the steel industry. This technology integration eliminates the need for intermediate processes such as slab reheating. By leveraging the advantages of a hot strip mill coupled to direct casting, we achieve cost savings, improve operational efficiency, enhance product quality and reduce environmental impact. As the DSPC is ideally designed to integrate into our new EAFs, we have transformed into a state-of-the-art mini mill production facility.

The DSPC enables us to offer superior products, meet customer needs more effectively and strengthen our position in the steel industry. This technology offers key advantages, including:

| • | Cost Efficiency: Direct casting eliminates the need for costly and time-consuming slab reheating processes. The continuous production method reduces energy consumption and operational costs associated with reheating furnaces, resulting in improved cost efficiency. |

| • | Time Savings: By eliminating intermediate processes, a hot strip mill coupled to direct casting significantly reduces the production cycle time. This allows for faster turnaround and shorter lead times, giving us a competitive edge in meeting customer demands and achieving just-in-time delivery. |

| • | Improved Quality: Direct casting technology allows for better control over our steel products’ microstructure and mechanical properties. The continuous casting process results in improved product consistency and surface quality, reducing defects and enhancing the overall quality of our steel products. |

| • | Environmental Benefits: The integration of direct casting minimizes the environmental impact of steel production by reducing energy consumption and greenhouse gas emissions. This aligns with sustainability goals and enhances our reputation as an environmentally responsible producer. |

| • | Flexibility and Customization: With a hot strip mill coupled to direct casting, we are able adapt to market demands more efficiently. The continuous process enables quick changes in steel grades, sizes, and specifications, allowing for greater flexibility and customization options to meet customer requirements. |

Discrete Plate Production

We are the only discrete plate producer in Canada, with current capacity of up to 700,000 tons per year.

Recent modernization of the Company’s 166-inch wide plate mill is expected to support annual plate production capacity of up to approximately 700,000 tons. The modernization, completed in 2024, enhanced rolling capability, dimensional tolerances, product quality and heat-treatment processing capability.

The Company produces a broad range of carbon-manganese, high-strength and low-alloy plate grades. Plate products are supplied in the as-rolled condition as well as in value-added heat-treated conditions, including normalized and quenched-and-tempered grades designed for demanding structural and industrial applications.

The Company’s plate products are used across a wide range of end markets including construction infrastructure (such as bridges and structural components), energy and pressure vessel applications, shipbuilding and marine equipment,

- 10 -

rail transportation equipment, heavy machinery and mining equipment, storage tanks and power generation equipment, large-diameter pipe and tubular products, and defense applications including armored plate. The primary end-users of the Company’s plate products are fabricators and manufacturers serving the construction, energy, mining, transportation, industrial and defense sectors. Plate steel products represented approximately 23% of the Company’s total steel shipment volumes for the twelve-month period ended December 31, 2025. The primary end users of the Company’s plate products are fabricators and manufacturers serving the construction, energy, mining, transportation, industrial and defense sectors.

Employment and Government Support

We are the largest employer in Sault Ste. Marie, Ontario. As of December 31, 2025, the Company had 2,400 full-time employees, of which approximately 95% are represented by two locals of the United Steelworkers Unions under two collective bargaining agreements expiring July 31, 2027. As discussed above, in connection with EAF Transition and the Company’s response to the S232 Tariffs, on December 1, 2025, the Company issued layoff notices to 1,005 unionized employees, effective March 23, 2026. As a result of the Company’s good relationship with its unionized workforce, there has not been a work disruption in approximately 30 years, and we have achieved contract terms that are competitive to those achieved by our peers.

As a result of our significant contribution to the Canadian steelmaking industry, we benefit from strong federal and provincial government support in various forms including the LETL Facilities. For example, to support political policies of the governments of Canada and Ontario, we have received financial support in the form of loans and grants, which have enabled us to undertake various capital expenditures to reinvest in the Company.

Environmental, Social and Governance

As part of our commitment to continue to augment our transparency and accountability on environmental, social and governance (“ESG”), the Company published its third annual sustainability report, (the “Sustainability Report”) in June 2025. Algoma aims to be a climate change leader and contributor toward a sustainable and environmentally responsible future for Canadian steel production. The report was designed to align with market-leading, investor-preferred ESG disclosure frameworks, such as the Sustainability Accounting Standards Board and the recommendations of the Task Force on Climate-related Financial Disclosures. The Sustainability Report sets out the Company’s ESG strategy, and its approach to mitigating ESG risks and capturing ESG opportunities, and provides an update on the Company’s ESG performance. We intend to publish our next report in June 2026.

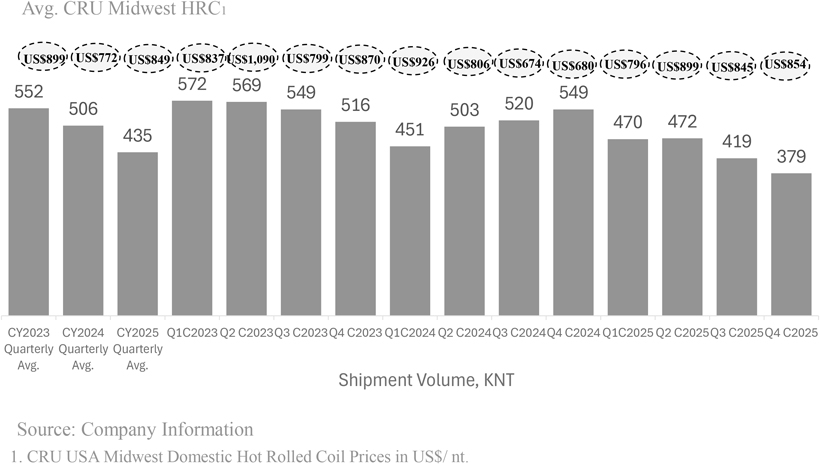

Quarterly Shipment Volume

- 11 -

Our Competitive Strengths

Strategically Located in Close Proximity to Customers and Suppliers

We are strategically located on Lake Superior with close proximity to major steel-consuming regions in Canada, including Southern Ontario, and historically to key markets in the United States, including the U.S. Midwest and Northeast. This geographic position has historically allowed the Company to serve customers across the Great Lakes region at competitive costs and, where trade conditions permit, provides strategic access to U.S. markets. Our location also provides efficient access to significant sources of post-consumer steel scrap, which is expected to be an important raw material input for our operations.

Historically approximately 84% of our customers are located within a 500-mile radius of our facility. In addition, our location on the Great Lakes provides access to multiple transportation modes, including marine, rail and truck, supporting our ability to negotiate competitive rates for inbound raw materials and outbound steel products. Our adjacent port facility, the fourth largest Canadian port on the Great Lakes by volume, has historically handled nearly 450 vessels per year and more than 4.5 million tons of shipments, facilitating efficient access to low-cost marine transportation across the Great Lakes and supporting our distribution network.

We sell steel products to a diverse base of approximately 235 customers across multiple sectors in North America, with no single customer accounting for more than 10% of revenues. Our top ten customers accounted for approximately 52% of total revenue in the year ended December 31, 2025. Our geographic, sector and customer diversification reduces our exposure to shifts in demand, and we have built strong customer relationships, with the average tenure of our top ten customers ranging from approximately 20 to 25 years.

The following map illustrates the Company’s advantageous location at the junction of Lake Superior and Lake Huron, with access to scrap metals anticipated to be sourced from the large industrial zones surrounding the Great Lakes (including Chicago, Detroit and Toronto), with additional supply from Western Canada and Quebec, and efficient shipping routes to customers throughout the Great Lakes region, including Canada and, where trade conditions permit, the Midwestern United States.

- 12 -

Operations Designed to Provide Superior Product Quality and Serve Diversified Blue-Chip Customer Base in Attractive End Markets

Plate products accounted for 23% of shipments, hot rolled sheet for 70% and cold rolled sheet for 7% of shipments for the twelve month period ended December 31, 2025. Additionally, flexible union labor contracts allow us to optimize manpower allocation across the entire facility to meet changes in demand. Our facilities have the flexibility to produce varying product widths, gauges and strengths, which allows us to serve a broad customer base across various end markets, including service centers, automotive, manufacturing, construction and tubular markets. Furthermore, our research and development investments support higher quality, lower cost products and drive a value proposition for customers.

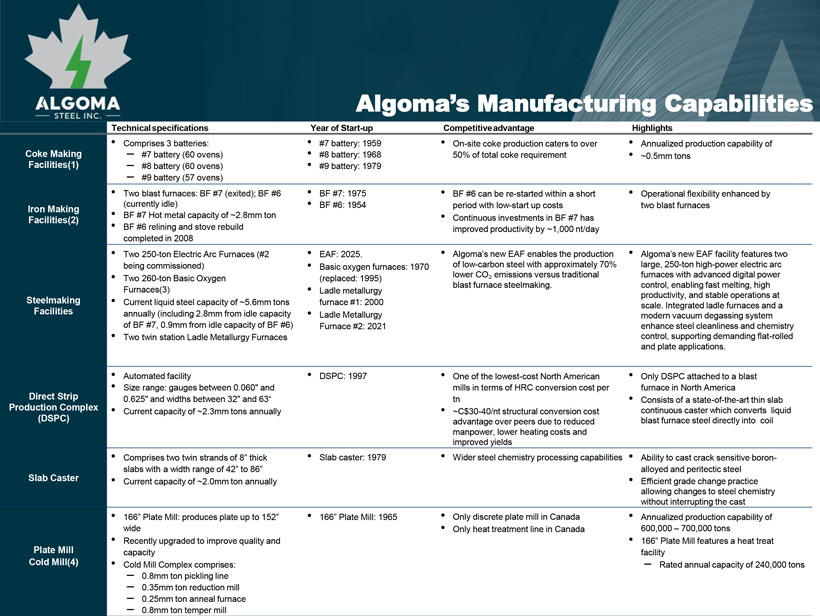

(1) Cokemaking Facility Closed January 2026; (2) No. 7 Blast Furnace Closed January 2026; (3) Basic

Oxygen Furnaces Closed January 2026; (4) Idled in January 2026 in response to U.S. tariffs

Source: Company information.

We serve a diverse and blue-chip customer base with over 235 customers across multiple industries in North America. No single customer makes up more than 10% of our sales. In the twelve month period ended December 31, 2025, 27% of our sales were to transportation customers (35-40% of which were in the automotive market), 21% of sales were to manufacturing and construction markets, 13% of sales were to tubular markets (primarily serving oil and gas customers), and 39% of sales were sold to distribution customers. Our geographical sales are divided between the

- 13 -

United States and Canada, serving high-quality industrial customers generally located on or near the Great Lakes given our logistical advantages. While the geographical sales mix varies year-by-year depending on relative demand, in the twelve month period ended December 31, 2025, 51% of our products were sold into the United States market while 48% were sold within Canada.

Low Cost Operations Underpinned by Scrap Flexibility and Stable Conversion Costs

As an EAF producer, we convert recycled ferrous scrap into steel, employing a flexible production model with a highly variable cost structure. This approach allows for alignment of raw material procurement, production, optimizing working capital, and reducing inventory risk. Underpinning this flexibility is a rigorous management of conversion costs. The Company strives to maintain consistent per-ton conversion costs, ensuring a resilient and competitive cost structure through-the-cycle.

During the EAF Transition and pending completion of local and regional 230 kV transmission upgrades, the Company supplements electricity supplied from the provincial grid with generation from its Lake Superior Power (“LSP”) facility. This capability provides operational reliability and flexibility while supporting grid stability during a period of transmission constraint.

Flexible Cost Structure Positions Algoma to Generate Cash Flow Through-the-Cycle

The combination of a flexible cost structure and the reduction in fixed costs positions the Company to potentially generate positive cash flow through the steel economic cycle, including at HRC prices significantly lower than in the current pricing environment.

Legacy Liabilities Sustainably De-Risked from CCAA Process

In connection with the Company’s acquisition of substantially all of the operating assets of the Algoma steelmaking business pursuant to a court-approved restructuring under the CCAA completed on November 30, 2018 (the “Restructuring Transaction”), the Company addressed certain legacy environmental liabilities associated with historical operations at its Sault Ste. Marie facility. As part of the Restructuring Transaction, the Company entered into an agreement with the Province of Ontario, as represented by the Minister of the Environment, Conservation and Parks (the “LEAP Agreement”), relating to historical soil, groundwater and sediment impacts at the site arising from more than a century of steelmaking activity. Under the LEAP Agreement, the Province provided the Company with a release from legacy environmental liabilities associated with historical contamination at the Sault Ste. Marie site. In exchange, the Company committed to fund C$3.8 million annually for a period of 21 years into a financial assurance fund to support approved legacy environmental remediation and related projects. The Company also provided a C$10 million letter of credit to the MECP as financial assurance for these obligations.

Experienced Management Team with Extensive Industry Experience

We have an experienced management team with significant operating experience in the global steel industry. Our executives collectively have almost 200 years of steel industry experience with a number of leading steel companies. Under the leadership of our current management team, we have made significant capital expenditures and have achieved significant operating performance improvements by employing benchmarking and implementing industry best practices. Furthermore, we maintain a strong relationship with our skilled unionized workforce, which allows us to benefit from favorable collective bargaining agreements that provide flexibility to adapt to changes in operational and production needs.

Products

Sheet Steel: Our flat/sheet steel products include a wide variety of widths, gauges, and grades, and are available unprocessed and with value-added processing such as temper rolling, cold rolled in both full-hard and annealed, hot-rolled pickled and oiled products, floor plate and cut-to-length products. The primary end-users of our flat/sheet products are the automotive industry, hollow structural tube manufacturers and the light manufacturing and transportation industries. For the last five years, sheet steel products have represented approximately 86% of our total

- 14 -

steel shipment volumes. Over the same period, value-added applications represented approximately 46% of total steel volume.

Plate Steel: Our plate steel products consist of various carbon-manganese, high-strength, low-alloy grades that are produced in as-rolled, hot-rolled and heat-treated. The primary end-user market of our as-rolled plate products is the fabrication industry, which uses our plate products in the construction or manufacture of railcars, buildings, bridges, off-highway equipment, and storage tanks. The primary end-user of our heat-treated plate products is ship building, defense industries, including armored products for military applications, as well as infrastructure and wind energy generation equipment. For the last five years, plate steel products have represented approximately 14% of our total steel shipment volumes.

Sales by Major Product Lines

Total sales, accounted for by each of our major product lines for the periods indicated below, were as follows:

| Twelve months ended | Nine months ended | Twelve months ended | ||||||||||

| December 31, 2025 | December 31, 2024 | March 31, 2024 | ||||||||||

| Sheet & Strip |

C$1,311.8 | C$1,346.7 | C$2,035.8 | |||||||||

| Plate |

565.8 | 324.1 | 506.2 | |||||||||

| Slab |

0.8 | 1.3 | 3.3 | |||||||||

| Freight |

175.3 | 142.7 | 198.3 | |||||||||

| Non-steel sales |

32.0 | 26.3 | 52.2 | |||||||||

| Total |

C$2,085.7 | C$1,841.1 | C$2,795.8 | |||||||||

Sales and Marketing

The principal markets for our products are steel service centers, the automotive industry, manufacturing and construction. We historically market our sheet and plate products mainly through distributors in Canada and the United States with growing exposure to the end use application. We are focused on leveraging various competitive attributes of our process and product technologies to improve market and customer segmentation. We pursue the development of applications and markets for our high strength and light gauge products to respond to application design factors. We are also focused on increasing the Company’s product portfolio to include more value-added products.

The Company pursues a diversified market and customer strategy to manage earnings volatility in the North American steel market. It is critical that a North American steel producer provide products to customers in all sectors of the economy given the industry dynamics, strong competition and global overcapacity. Focusing on more than one commodity to one sector is key to ensuring earnings stability through the business cycle and achieving greater stability in economic downturns. The Company believes it has strong customer loyalty which helps it to manage through the volatility of the steel pricing cycle.

The distribution of total steel revenue by principal markets for the periods indicated below, was as follows:

Total North American Revenue by Major Markets

- 15 -

| January 1, 2025 to December 31, 2025 |

April 1, 2024 to December 31, 2024 |

April 1, 2023 to March 31, 2024 |

||||||||||

| % | % | % | ||||||||||

| Steel service center |

39 | 18 | 17 | |||||||||

| Transportation1 |

27 | 41 | 43 | |||||||||

| Manufacturing & Construction |

21 | 28 | 30 | |||||||||

| Tubular and other |

13 | 13 | 10 | |||||||||

| Total |

100 | 100 | 100 | |||||||||

| 1Includes 35-40% automotive |

||||||||||||

Competition

The global steel industry is highly competitive and characterized by significant production capacity. There has been a substantial increase in global steelmaking capacity over the past two decades, particularly in China, which is now the largest producer and consumer of steel in the world. Periods of slower domestic economic growth in China or production levels that exceed domestic consumption may result in surplus steel being exported into international markets, including North America.

Trade measures in the United States have also affected competitive dynamics in the North American steel market. Tariffs and other trade restrictions imposed by the United States on steel imports have curtailed direct imports into the U.S. market, which may result in foreign producers seeking alternative export markets, including Canada. This trade diversion has increased competition from rest-of-world (“ROW”) steel imports into the Canadian market. Canadian trade policies, including the use of tariff rate quotas, safeguard measures and remission frameworks applicable to certain products and countries, have provided some support to domestic producers; however, these measures have not fully mitigated the impact of increased import competition in Canada.

We compete with numerous domestic and foreign steel producers, including both integrated producers and EAF producers. Competition is primarily based on delivered price, product quality, reliability of supply and customer service. EAF producers typically require lower capital expenditures for construction and maintenance of facilities and may operate with lower employment costs; however, these advantages may be reduced when scrap prices are elevated.

The Company operates as an independent steel producer. Certain of our competitors in the North American market are subsidiaries of large multinational steel producers or industrial groups with operations across multiple jurisdictions. These organizations may benefit from broader access to capital, internal supply chains, global procurement networks and coordinated commercial strategies across affiliated operations, which may enhance their ability to compete in certain markets.

Although freight costs for steel products can limit competition from distant producers, foreign producers with lower labor, raw material or energy costs, or those benefiting from government support or subsidies, may still compete effectively in our markets, particularly on the east and west coasts of Canada. Increased imports into North America could result in downward pressure on domestic steel prices, which could adversely affect our revenues, margins and profitability.

Our competitive position benefits from our location on the Great Lakes, which provides access to efficient marine transportation for both inbound raw materials and outbound finished steel products. Approximately 84% of our customers are located within a 500-mile radius of our facility in key steel-consuming regions of the Midwest and Northeast United States and southern Ontario, enabling us to serve customers at competitive transportation costs. As is common industry practice, we may assume additional shipping costs in certain circumstances in order to remain competitive in markets outside our immediate geographic region.

- 16 -

Trade

Our business has been materially impacted by tariffs and other trade restrictions imposed on steel exports from Canada to the United States (see “The Company’s Response to Tariffs”). Historically, the United States has been a strategically important market for the Company given our geographic proximity to major industrial regions in the U.S. Midwest and Northeast and the integrated nature of the North American steel market. Measures that materially restrict or effectively close access to the U.S. market may significantly reduce the Company’s ability to sell products into that market.

Tariffs imposed by the United States on imported steel and certain derivative steel products have created uncertainty regarding the Company’s ability to access the U.S. market. If such measures persist or are expanded, they may materially limit or prevent the Company from exporting steel products to the United States for an extended period. In addition, tariffs imposed by the United States on steel imports may redirect steel exports from other countries into alternative markets, including Canada. Such trade diversion can increase the volume of foreign steel entering the Canadian market, potentially leading to increased supply and downward pressure on domestic pricing and demand. These factors could adversely affect the Company’s financial condition and results of operations.

The Canadian government has imposed retaliatory surtaxes on certain steel products imported from the United States. The government has also issued remission orders exempting certain products, businesses and applications from these surtaxes, which may reduce the overall effectiveness of these measures in protecting the domestic steel market.

USMCA, which came into force in July 2020, governs trade among Canada, the United States and Mexico. The agreement includes provisions requiring higher levels of North American automotive content, including steel, for vehicles to qualify for duty-free treatment and requiring that at least 70% of steel used in automobiles be melted and poured in North America. The agreement will undergo its first six-year review in July 2026, at which time the parties will assess its operation and consider potential amendments. The agreement also contains a sunset provision under which it will terminate in 2036 unless the parties agree to extend it. The upcoming review process, and the possibility of renegotiation or modification of certain provisions of the agreement, creates additional uncertainty regarding the future trade framework governing steel trade within North America.

Our business has historically been affected by the importation of steel products into North America at prices below cost or below prices prevailing in the exporting country’s domestic market (“Dumping”). Dumping may result in suppressed prices, lost sales, reduced profitability and lower production levels for domestic steel producers. In some cases, foreign steel producers are owned, controlled or supported by their governments, and production decisions may be influenced by policy objectives rather than market conditions, contributing to global excess steel capacity. In addition to Dumping, we compete with imported steel products that may be offered at material discounts to prevailing market prices in our principal markets. These imports may place downward pressure on domestic pricing and reduce margins for domestic producers.

Recent trade dynamics have also contributed to a divergence between Canadian steel pricing and broader North American pricing benchmarks. While key input costs for EAF steelmaking, including scrap, are generally priced based on North American indices, increased import competition in Canada may result in domestic steel prices that are lower than prevailing prices in other North American markets. This pricing disconnect may adversely affect margins for Canadian steel producers.

Over time, the Canadian and U.S. steel industries have successfully pursued trade remedy actions to address unfairly traded imports. Although these measures have reduced certain import volumes, they may not be sufficient to prevent future unfair import pricing practices. Weakening of Canadian or U.S. trade laws, or the expiration or modification of existing trade remedies, could increase imports into North American markets and materially adversely affect our business and financial performance. There remain numerous anti-dumping and countervailing duty findings covering imports of hot rolled sheet, cold rolled sheet and plate products into both Canada and the United States from various countries, including China, India, South Korea and other jurisdictions. These trade measures are intended to mitigate the effects of unfairly traded imports but may not fully eliminate competitive pressures from global steel producers.

- 17 -

The Company continues to monitor imports of competing steel products into its markets and may pursue appropriate trade remedies where warranted.

The Government of Canada has implemented several additional measures since late 2024 intended to address offshore steel imports:

| • | October 22, 2024: Canada imposed an additional 25% surtax on certain steel and aluminum products produced in China and imported into Canada, in addition to existing anti-dumping and countervailing duties. |

| • | July 31, 2025: The surtax was expanded to apply to certain products manufactured using steel melted and poured in China. |

| • | June 27, 2025: Canada introduced tariff rate quotas (“TRQs”) on imports of certain steel products from countries other than Canada’s USMCA partners. These TRQs have subsequently been amended to adjust covered product categories and restrict quota volumes, including reductions in allowable import levels and surtaxes on over-quota imports and certain derivative steel products. |

The Canadian government also retains the authority to issue remission orders that may reduce the application of certain trade measures.

Information Systems

Our information technology landscape supports a high level of business automation across three distinct segments of business processes: management decision systems, manufacturing execution/scheduling systems and process control systems. Our management decision systems, including the full order-to-cash cycle, are running on the SAP (Windows/Oracle) platform. Our manufacturing execution/scheduling systems run on the IBM mainframe environment. Our process control systems run on Windows, Vax, and Honeywell environments. Our infrastructure includes a LAN/WAN data network, desk/mobile phone services, approximately 650 physical/virtual servers, approximately 1,200 PCs and two main datacenters (SAP at the Sault Ste. Marie, ON and Mainframe at Markham, ON). Daily incremental and full back-ups, including offsite replication and storage, are created for disaster recovery purposes.

Enterprise Risk Management

The Company employs an enterprise risk management (“ERM”) process to coordinate risk management among departments to manage the organization’s full range of risks as a whole. ERM offers a framework for effectively managing uncertainty, responding to risk and harnessing opportunities as they arise. A comprehensive ERM framework consolidates and improves risk reporting to identify key risks that may affect the Company, quantify and manage them better, and implement the proper controls to eliminate or reduce the threat.

Algoma employs an enterprise risk management program that proactively identifies and manages strategic risks to the organization. ERM follows a very distinct and ongoing process, where it actively identifies and reassesses the various strategic and major risks to ensure financial security for our business. The framework leverages systemization of the risk registers for prioritization and tracking; and applying effective mitigation strategies to manage risks. The ERM program extends its reach to evaluate strategic decisions and plans for the organization, as well as developing a risk culture to ensure longevity and sustainability of Algoma’s competitiveness.

Growth Strategies

In addition to our strategic goals focused on the ramp-up of our EAF Transformation and other key investment projects, we are constantly focused on applying a forward-looking value-focused lens on growth, increasing our participation in key sustainable markets, generating a competitive return on capital, and meeting our financial and other obligations for all stakeholders. The Company is exploring alternative products and income streams as means to diversify from traditional cyclical steel commodity exposure.

- 18 -

We are committed to improving our quality, cost competitiveness and customer service, as well as developing a diverse organization to support our long-term success, while maintaining safety excellence and environmental stewardship as key performance objectives.

Continuous Margin Stability Enhancement and Cost Improvement. We are striving to continue reducing our costs and improving our operating performance. Cost improvements include maintenance effectiveness, operations reliability, operational cost reductions, workforce effectiveness, power efficiency improvements, process yield improvements, improvements in product quality and optimization of gas usage.

Capitalize on Low-Cost Growth Opportunities. Our goal is to continue enhancing our productivity and profitability through prudent capital investment projects, and we will continue to evaluate opportunities of this nature. The LMF2, which debottlenecked our process flow and the additional capacity that we anticipate to add with our plate mill modernization, are strong examples of how we seek to deploy capital to high return projects.

Maintaining a Prudent Financial Policy. We are committed to maintaining a strong financial profile for the Company. Our management is focused on generating disciplined growth while maintaining a strong credit profile, limiting net long-term debt and enhancing liquidity. The Company seeks to maintain adequate cash and available liquidity throughout the seasonality in its business cycle.

Additionally, our capital allocation strategy is focused on low-cost growth opportunities to enhance the capabilities and low-cost operating position of our steel mill and related works. These investments include the development of our EAF and internal investments such as the LMF2 debottlenecking project and the plate mill modernization.

Focus on Safety and Environmental Compliance. Management remains firmly committed to maintaining safe, healthy, and environmentally responsible operations. We continue to advance initiatives that enhance worker health and safety, strengthen environmental performance at the plant level, and support the wellbeing of the broader community. As part of this commitment, we have significantly reduced our carbon footprint and, as of January 2026, eliminated coke oven emissions through the cessation of operations at our #7 Blast Furnace and all three coke oven batteries. Our focus on safety has also delivered measurable results. Since the fiscal year ended March 31, 2015, we have reduced our Lost Time Injury Frequency Rate (LTIFR) - measured as lost time incidents per 200,000 hours worked - from 0.72 to approximately 0.16 for the calendar year ending December 31, 2025. The wellbeing of our employees and the communities in which we operate remains our highest priority, as reflected in our core values: Safety, Teamwork, Integrity, and Caring.

We are committed to being responsible environmental stewards and encourage open communication and reporting to our communities with regard to our environmental performance. Through our participation in the Canadian Steel Producers Association, we have committed to pursue the aspirational goal of carbon neutrality by 2050. We continue to evaluate and pursue strategies to both meet this goal and maintain our competitiveness, including through the modernization of our existing facilities and the adoption of other technologies such as less carbon-intensive iron making or EAF steelmaking. We estimate that the transition to EAF steelmaking will result in a reduction of 3.0 million tonnes of CO2 emissions per year, representing a 70% reduction to historical emissions levels with a goal of eliminating all coal use in our steelmaking operations over time, which we believe will allow us to become one of the greenest producers in North America and reduce the potential impact of the Canadian carbon tax regime on our business.

All of our facilities are qualified under the global ISO 14001 Environmental Management System Standard. We are supporting open dialogue on environmental issues with the community by establishing community outreach initiatives and ensuring frequent reporting on our environmental performance. For example, we have established a Community Liaison Committee as a forum for exchanging relevant environmental information with the public, conducting meetings on a quarterly basis and publishing meeting notes on our website.

The Company instituted an environmental community liaison committee (“CLC”) to solicit representation from community organizations, agencies and public bodies, with the objective of keeping the local community informed about the operations of our facilities in relation to environmental regulations in effect, and to keep the Company informed of any community concerns about the operations of our facilities.

- 19 -

The CLC also serves as a forum for dissemination, review and exchange of information related to the environmental impact of our facilities. In order to ensure the objectives of the CLC are met, the Company provides information to the members as necessary on an ongoing basis.

Sources and Availability of Raw Materials

EAF steel production requires the use of large volumes of bulk raw materials and energy, in particular ferrous scrap, as well as natural gas, electricity, alloys, oxygen, and other inputs, the prices of which can be subject to significant fluctuation. The prices of ferrous scrap can vary greatly from time to time. Prior to becoming an EAF producer, our results have historically been impacted by movements in coal and iron ore prices. Iron ore and coal prices have been volatile in recent years.

Scrap Metal and Iron Units

In 2021 we entered into a joint venture with Giampaolo Group Inc., the parent company of Triple M Metal LP and one of North America’s largest privately owned ferrous and non-ferrous metal recycling companies, establishing a jointly owned company known as ATM Metals Inc. The new entity sources prime scrap metal and other iron units to meet the Company’s business needs, including in connection with its transformation to EAF steelmaking.

Other Raw Materials

We purchase limestone, alloys and other raw materials for our manufacturing operation at what we believe to be competitive prices. We generate a portion of our scrap requirements internally and the balance is purchased from third parties, primarily from regional sources where we have a pricing advantage over other markets due to our proximity to the suppliers.

Energy

We purchase all of our natural gas from independent suppliers at market pricing. We may use fixed price contracts to manage exposure to natural gas price changes traditionally seen during peak winter months (January to March). We purchase under both variable and fixed price contracts for both volume and delivery.

As an EAF producer, we purchase our electricity needs from the Independent Electricity System Operator in Ontario supplemented with our internal natural gas-fired LSP generation facility. We also are eligible for electricity rebates under the Northern Energy Advantage Program.

Oxygen is supplied by Linde Canada Inc. through a supply agreement that extends to mid-2026.

See “Risk Factors – Electricity supply constraints and power costs in Northern Ontario could adversely affect our operations and financial performance..”

Government Regulation

The Company’s environmental policy is to conduct our business in a manner that ensures the Company and its personnel act reasonably and responsibly within applicable legislation and regulations with respect to the protection of the environment. Where appropriate, we have introduced environmental accountability to all employees. Activities that may have an impact on the natural environment have been identified and managed through the implementation of our ISO14001 compliant environmental management system. Our Environment Department regularly reviews and audits our operating practices to monitor compliance with our environmental policies and legal requirements.